Starting A 529 Account Early

Welcome to Saving Money with Andrew!

Almost a year and a half ago, I first sang the praises of 529 college savings accounts.[1] These accounts, which let you save tax-free for education expenses for kids and other family members, combine some of the best features of other tax-advantaged savings vehicles, such as IRAs and 401(k)s. Contributions grow tax-free, provided that the funds are ultimately used for qualifying educational expenses. And as an added bonus, about 30 states provide a state income tax deduction for contributions.

One of the most important things to realize about these accounts is that you don’t have to have children to open one, as a helpful reader recently noted. As a result, these are also worth considering if you are looking for a tax-advantaged way to save for the future, have already maxed out your IRA (or 401(k), if you have one), and think there is a good chance you will have a child someday.

Most people are familiar with 401(k)s (60 million active participants in the US with $6.9 trillion in assets) and IRAs (over 45 million households in the US with $12.6 trillion in assets). This is for good reason—for those able to contribute, the tax benefits of these accounts are very compelling, even if one’s employer does not offer a matching contribution.

Far fewer are familiar with 529 Savings Plans (nearly 15 million accounts with over $400 billion in assets). Included among these accountholders are the Obamas, who made a large contribution to their own 529 Plan in 2007. These plans, created by Congress in 1997, allow individuals to save money for their own or others’ education expenses by contributing to a “529 Savings Plan”. These plans offer three great benefits:[2]

In the majority of states, contributions up to a certain limit are tax-deductible from your state taxes. For example, in New York, those in the 6.33% tax bracket save ~$317 on their tax bill for making a $5000 contribution.

Investment income in a 529 Savings Plan is not taxed until withdrawal

Withdrawals from a 529 Savings Plan are tax-free if used for qualified education expenses.[3] Other withdrawals are subject to tax and a 10% penalty (but only on the income, not on the original contribution)

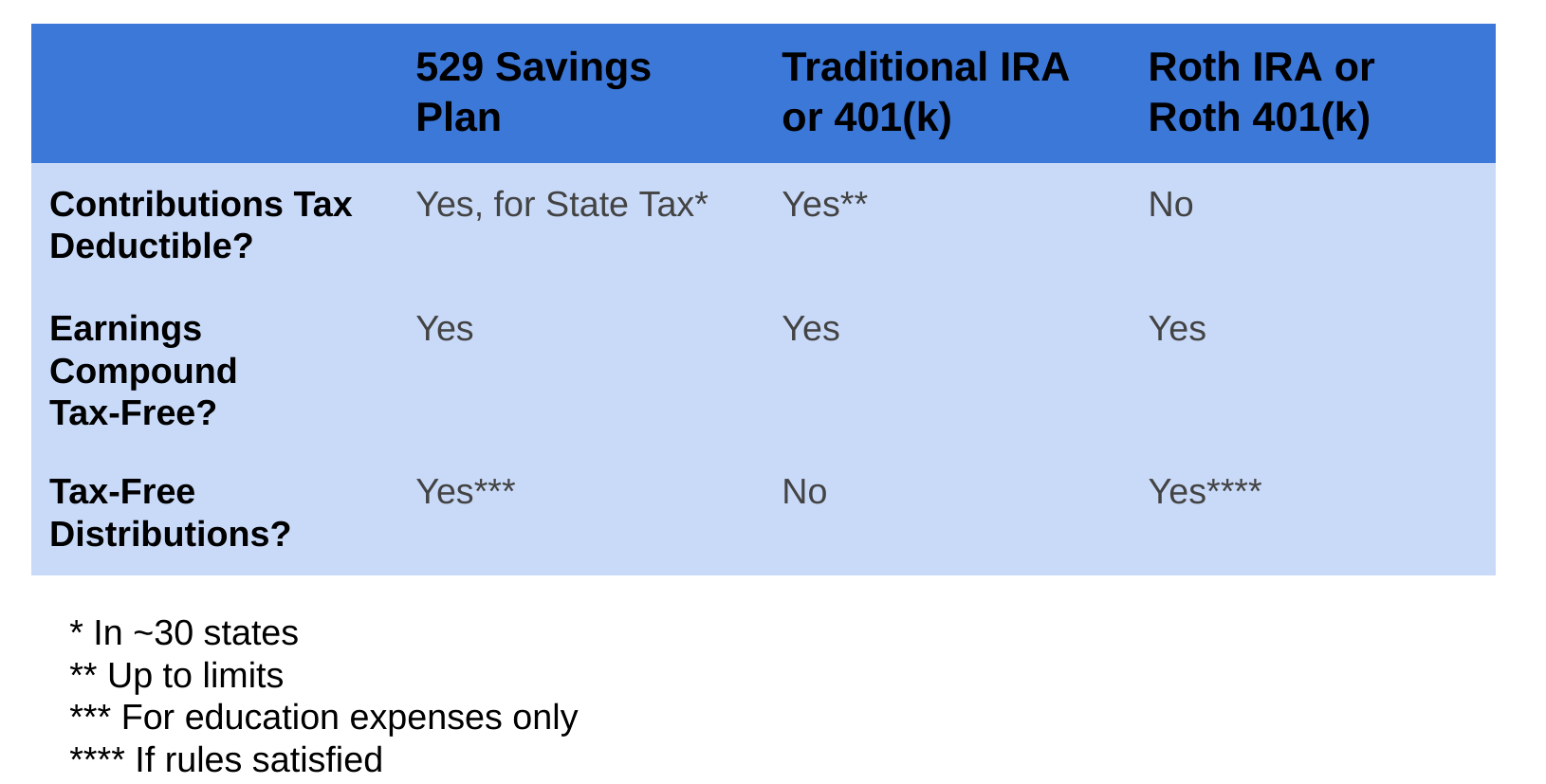

Here’s a helpful table comparing 529 plans to IRAs and 401(k)s:

Essentially, as long as you use the 529 to pay qualified education expenses, it combines the tax benefits of a Roth 401(k) or Roth IRA (tax-free distributions) with an additional upfront bonus of a state tax deduction (in ~30 states).

To get started, find the 529 savings account provider for your state. Make sure to review the fees charged by the plan provider (they often vary significantly from state to state).

These plans are well-worth considering for parents, and there are many others who might find a 529 very interesting as well, including:

Grandparents who want to save for their grandkids’ educations, while still maintaining control of the account and investments (and getting a tax benefit)

Singles and childless couples who intend to have kids someday. In most situations, you can open an account with yourself as beneficiary, and just change it down the road.[4] You could even use the funds for your own educational expenses, or for another relative.

By contrast, 529s make less sense for those who don’t intend to have children. Otherwise, 529 accounts are well-worth considering, especially if you are already “maxing out” other retirement accounts. As always, consult your accountant or financial adviser when making a big decision like this.

And now…Andrew’s pick of the week:

Ronan Farrow and Jia Tolentino have teamed up to write a gripping account of the Britney Spears crisis in the New Yorker. A great companion piece to this is the 2017 New Yorker piece on elder abuse in the guardianship system.

I hope this has been helpful. If you liked it, please share it on social media! Also, please send me your feedback, requests, and success stories.

[1] Since the vast majority of SMwA’s readers (about 80%) weren’t subscribers 18 months ago, I have updated this post a bit and am re-running it today.

[2] There are other significant potential estate planning benefits, as well as financial aid planning, but those are well beyond the scope of this post.

[3] Including college tuition, of course, but also certain related expenses. Recent changes offer limited ability to use 529 money for K-12 tuition and loan repayment, but these rules are complicated and may vary by state.

[4] Keep in mind that while the beneficiary can be changed, there may be tax issues if the account is large and the new beneficiary is in a different generation from the previous one. Consult your accountant if you’re in this situation.