Inflation, Inflation, Inflation

Welcome to Saving Money with Andrew!

Surging inflation has become a major political issue. 6% of Americans (enough to swing an election) list it as our most important problem, it has torpedoed President Biden’s domestic agenda, and it has eaten up a large portion of recent wage gains.

In 2021, inflation was 7%, the highest level since 1982.

Almost everything is more expensive:

The romaine in my Sweetgreen salad? Inflated.

Used cars? Really inflated. A sign of the times—we were recently offered as much for our two-year old car as we paid for it. Great…but then we’d need to find another car.

And those delicious Tagalong Girl Scout cookies? Inflated (and the box seems awfully small these days).

Here are a few things we’ve done to cope with inflation and higher prices:

Store Brands

Amid high inflation, consumers have shifted aggressively toward store brands. For anything without a discernible quality difference, we always go for the store brand and you should too.[1] You can find particularly attractive savings opportunities on over-the-counter (OTC) drugs and baby supplies, and also on almost all basic food items.[2] One can easily save hundreds of dollars this way.

I Bonds

US government “Series I” savings bonds pay a variable interest rate based on changes in the CPI, resetting every six months based on current inflation. Interest is state and local tax-free, and bonds are redeemable after one year (with a 3 month interest penalty) or after five years with no penalty.[3] I bonds currently yield over 7% and are quite popular lately, with more bonds sold last month than any individual year on record.

Loans

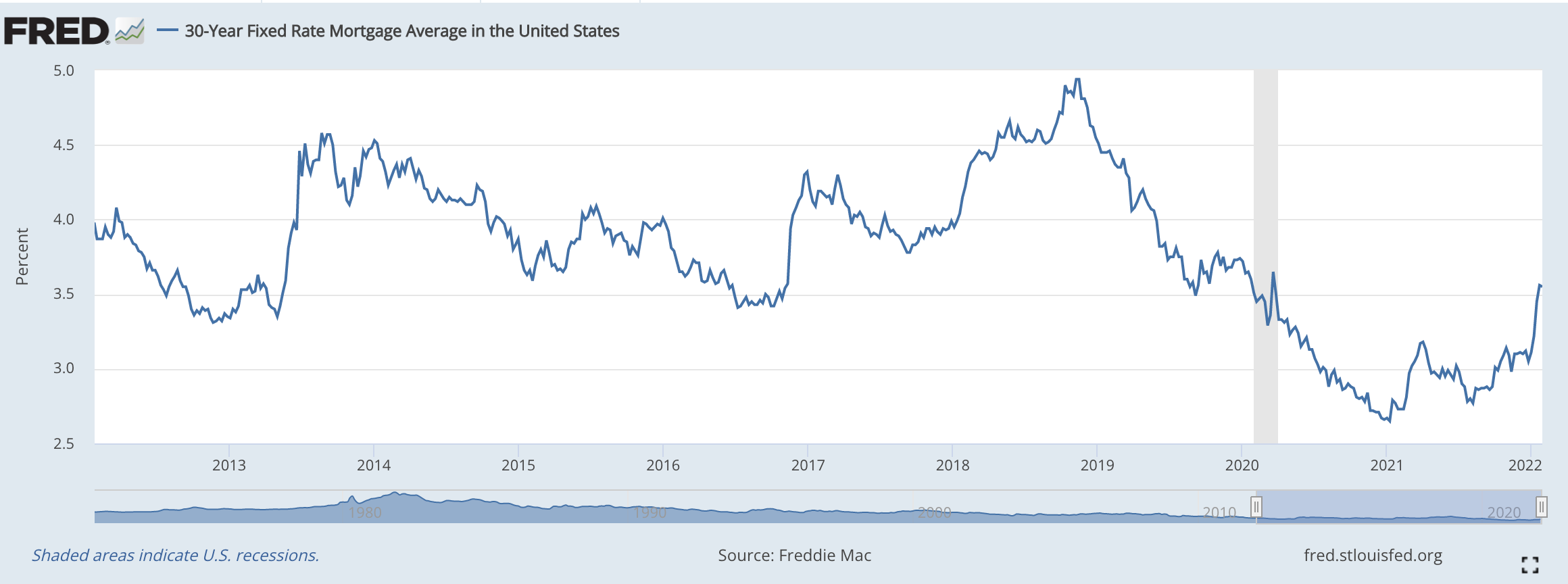

If you have low interest rate loans (for example, a mortgage under 4%), you probably want to pay them off as slowly as possible. Inflation is bad for assets, but is great for borrowers because it decreases the “real” value of your debt.

We may never again see the mortgage rates we saw last year, which bottomed at 2.65% for a 30 year mortgage and have since rebounded to 3.55% (still a great rate). So unless you truly have nothing more productive to do with the money, or just really want to have less debt, you might as well just make your required payments and not prepay.

And now…Andrew’s pick(s) of the week:

How It Feels to Be an Asian Student in an Elite Public School. An honest, objective, and thought-provoking article about the debate over NYC’s “exam schools”

Are You A Super Recognizer? (a 15-20 minute test, but kind of fun). Plus a good interview with a super recognizer.

Finally, three extremely fun videos of the top songs of the 1960’s, 1970’s, and 1980’s:

I hope this has been helpful. If you liked it, please share it on social media! Also, please send me your feedback, requests, and success stories.

[1] I discussed store brands at length in an early SMwA issue.

[2] From my earlier post:

The strongest support for always considering private label comes from a study from business professors at Brown, University of Chicago, and Stanford. According to their research, the more savvy the shopper, the more likely they were to choose a private label product. That is, the pharmacists bought the store brand medication 91% of the time (versus 74% on average) and the chefs bought the store brand salt, sugar, and baking soda 77% of the time (versus 60% on average).

[3] Note, this newsletter is *not* investment advice.